The Ultimate Real Estate Buying Guide for 2026

Your comprehensive real estate buying guide covering every step from pre-approval to closing. Buy smarter with your AI-powered home buying advisor.

Buying real estate is likely the biggest financial decision you'll make. Whether you're a first-time buyer or a seasoned investor, having a solid game plan makes all the difference between a smooth transaction and a stressful ordeal.

This comprehensive real estate buying guide walks you through every step of the process—from getting your finances in order to collecting the keys to your new home. And with Homecoming—your AI-powered home buying advisor—you'll have the insights to buy smarter and buy confident.

Quick Stats: The Home Buying Journey

- Average time from search to close: 4.3 months

- First-time buyers: 32% of all purchases

- Buyers who found their home online: 97%

- Average down payment (first-time): 8%

- Buyers who used an agent: 86% Source: National Association of Realtors, 2025

Before You Start: Financial Preparation

Check Your Credit Score

Your credit score determines the interest rates you'll qualify for—and whether you'll qualify at all. Before shopping for homes:

- Pull your credit reports from all three bureaus (Equifax, Experian, TransUnion)

- Dispute any errors that could be dragging down your score

- Pay down credit card balances to below 30% of your limits

- Avoid opening new accounts or making large purchases

A score of 740+ gets you the best rates. Between 620-740, you'll qualify but pay more. Below 620, consider spending 6-12 months improving your credit before buying.

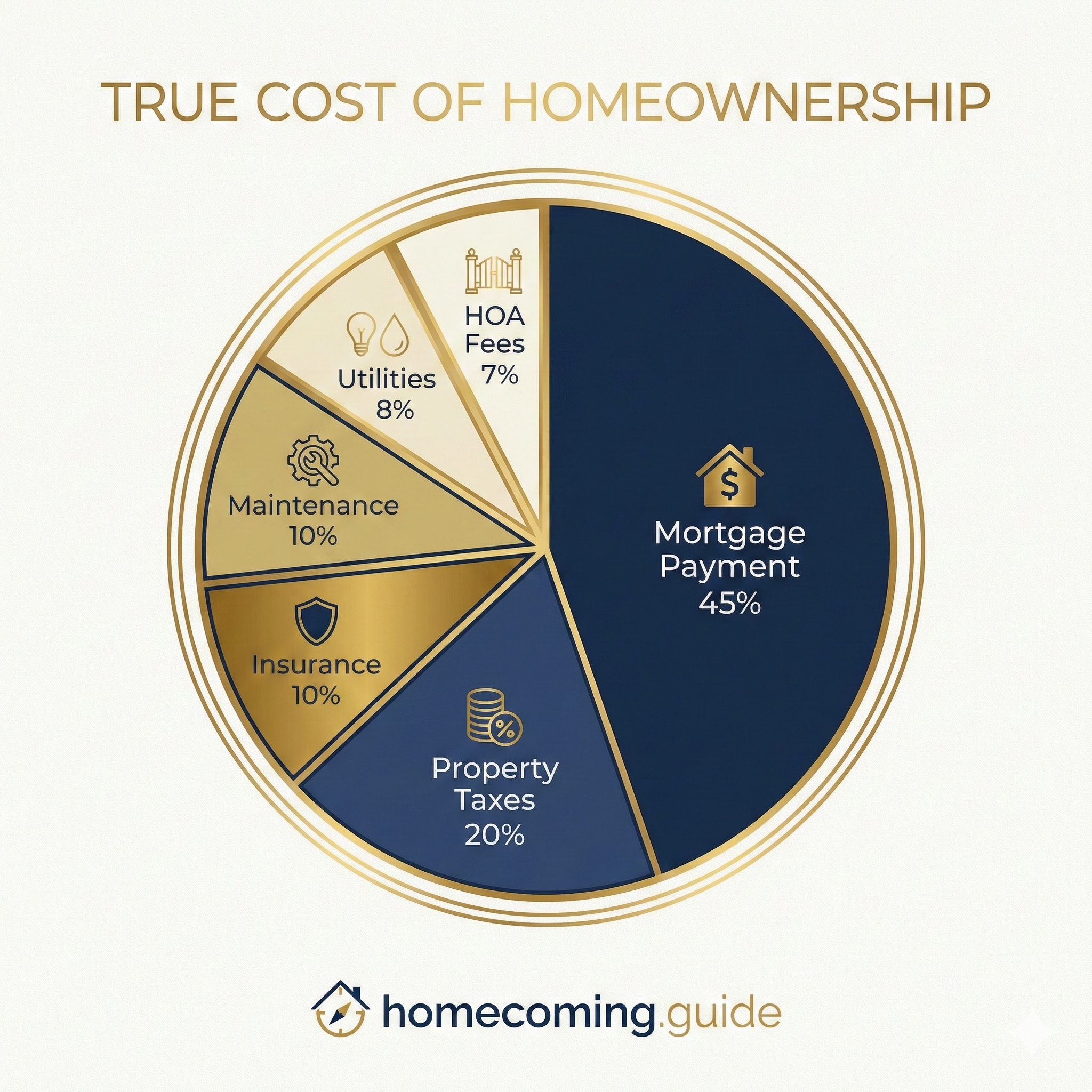

Calculate Your True Budget

Lenders will tell you the maximum you can borrow. That's not the same as what you should spend. Factor in:

| Monthly Costs | Description |

|---|---|

| Mortgage payment | Principal + interest |

| Property taxes | Varies by location (0.5% - 2.5% annually) |

| Home insurance | $1,000 - $3,000+ per year |

| HOA fees | If applicable |

| Maintenance | Budget 1-2% of home value annually |

| Utilities | Often higher than renting |

A comfortable mortgage payment is typically 25-28% of your gross monthly income—not the 43% lenders might approve.

Save for More Than the Down Payment

You'll need cash for:

- Down payment: 3-20% depending on loan type

- Closing costs: 2-5% of purchase price

- Reserves: 2-6 months of mortgage payments

- Moving expenses: Often overlooked but significant

- Immediate repairs or upgrades: The stuff you'll want to fix right away

Step 1: Get Pre-Approved

Pre-approval is your ticket to serious house hunting. It shows sellers you're a qualified buyer and helps you understand exactly what you can afford.

What Lenders Look At

- Income and employment (typically 2 years of history)

- Assets and savings

- Debt-to-income ratio

- Credit history and score

- Down payment source

Pre-Approval vs. Pre-Qualification

Pre-qualification is a quick estimate based on self-reported information. It's a starting point, not a commitment.

Pre-approval involves a full credit check, income verification, and conditional loan commitment. This is what you need before making offers.

Get pre-approved with at least 2-3 lenders to compare rates and terms. The credit inquiries within a 45-day window count as one inquiry for scoring purposes.

Step 2: Define Your Priorities

Before touring homes, get clear on what you need versus what you want.

Must-Haves (Non-Negotiable)

- Number of bedrooms/bathrooms

- Location (commute, school district, neighborhood)

- Minimum square footage

- Accessibility requirements

- Garage or parking needs

Nice-to-Haves (Flexible)

- Updated kitchen/bathrooms

- Outdoor space

- Specific architectural style

- Extra features (pool, finished basement)

Deal-Breakers

- Maximum commute time

- Busy road or commercial adjacency

- HOA restrictions that don't fit your lifestyle

- Issues you're not willing to fix

Write these down and refer back when emotions run high during the search.

Step 3: Find the Right Real Estate Agent

A good buyer's agent is worth their weight in gold. They know the market, spot problems, and negotiate on your behalf.

What to Look For

- Local expertise: They should know your target neighborhoods intimately

- Full-time commitment: Part-time agents may not be available when you need them

- Communication style: Do they respond quickly? Listen to your concerns?

- Track record: Ask about recent transactions similar to yours

Questions to Ask

- How many buyers have you represented in the past year?

- What's your experience in [specific neighborhood]?

- How do you handle multiple offer situations?

- What happens if we disagree on strategy?

Interview at least three agents before committing. In most markets, the seller pays the buyer's agent commission, so this representation costs you nothing directly.

Step 4: Search Strategically

Online Research

Start with major listing sites, but don't stop there:

- Set up saved searches with email alerts

- Track how long listings stay on market

- Note price reductions and patterns

- Research neighborhood crime, schools, and development plans

In-Person Tours

When viewing homes:

- First visit: Get the overall feel. Does it flow? Is the location right?

- Second visit: Look more critically. Check storage, natural light, noise levels

- Bring a tape measure: Furniture fit matters

- Visit at different times: Evening traffic, weekend activity

Take photos and notes—after a few homes, they start to blur together.

Step 5: Make a Strong Offer

When you find the one, move quickly but strategically.

Know the Market

- Seller's market: Homes sell fast, often above asking. You may need to waive contingencies or escalate.

- Buyer's market: More inventory, longer days on market. You have negotiating room.

- Balanced market: Reasonable negotiations, typical contingencies expected.

Offer Components

| Element | Description |

|---|---|

| Price | Based on comps, condition, and market |

| Earnest money | Shows commitment (1-3% typical) |

| Contingencies | Inspection, financing, appraisal |

| Closing timeline | When you'll complete the purchase |

| Inclusions | Appliances, fixtures, personal property |

Competing Against Multiple Offers

If you're up against other buyers:

- Get pre-approved, not just pre-qualified

- Offer strong earnest money

- Be flexible on closing date

- Write a personal letter (where legal and appropriate)

- Escalation clause: Automatically increase your offer up to a maximum

But know your limits. FOMO is expensive.

Step 6: Conduct Due Diligence

Once your offer is accepted, the clock starts on your contingency periods.

Home Inspection

Never skip this. A qualified inspector examines:

- Structural components (foundation, framing, roof)

- Major systems (HVAC, plumbing, electrical)

- Safety issues (smoke detectors, handrails, egress)

- Exterior (siding, drainage, grading)

Attend the inspection. Ask questions. Understand what you're buying.

Specialized Inspections

Depending on the property, you may also need:

- Sewer scope: Critical for older homes

- Radon testing: Required in some areas

- Pest inspection: Look for termites and other wood-destroying organisms

- Pool/spa inspection: If applicable

- Environmental testing: Lead, asbestos, mold

Review Disclosures Carefully

The seller's disclosure reveals known issues with the property. Read it thoroughly—this is where problems often hide in plain sight.

Did You Know? According to the National Association of Realtors, 86% of buyers used an agent to purchase their home, but only 38% felt they fully understood their disclosure documents before signing.

How Homecoming Puts You in the Driver Seat

This is where your AI-powered home buying advisor makes a difference. Upload your disclosure documents to Homecoming and get:

- Instant risk identification — Red flags highlighted within minutes

- Plain-language explanations — Legal jargon translated to understandable terms

- Cost estimates — Potential repair costs for disclosed issues

- Custom inspection checklists — Based on what's in your specific disclosure

- Comparison tools — Evaluate multiple properties side-by-side

Instead of hoping you didn't miss something buried on page 12, you'll know exactly what requires attention. Buy Smarter. Buy Confident.

Step 7: Negotiate Repairs

After inspection, you'll likely have a list of issues. Not everything warrants negotiation, but significant problems do.

Focus on:

- Safety hazards: These should be addressed before closing

- Major system failures: HVAC, plumbing, electrical, roof

- Structural issues: Foundation problems, water intrusion

- Code violations: Unpermitted work, missing safety features

Skip:

- Cosmetic issues

- Normal wear and tear

- Minor maintenance items

Request repairs or credits—credits often give you more control over the work quality.

Step 8: Final Financing

With inspections complete, your lender finalizes the loan.

Appraisal

The lender orders an appraisal to confirm the home is worth the purchase price. If it comes in low:

- Negotiate a lower price with the seller

- Pay the difference in cash

- Challenge the appraisal with additional comps

- Walk away (if you have an appraisal contingency)

Final Underwriting

Don't make any financial changes between pre-approval and closing:

- No new credit applications

- No large purchases

- No job changes

- No moving money between accounts without documentation

Any of these can derail your loan at the last minute.

Step 9: Closing

The finish line. Here's what happens:

Before Closing Day

- Final walkthrough: Verify the property is in agreed-upon condition

- Review closing disclosure: Compare to your loan estimate; question any changes

- Wire funds: Never wire money based on email instructions alone—call your title company to verify

At Closing

You'll sign a mountain of documents:

- Promissory note (your promise to repay)

- Mortgage/deed of trust (secures the loan with the property)

- Closing disclosure (final loan terms and costs)

- Title documents

Bring government ID and any required funds (typically a cashier's check for the remaining down payment and closing costs).

After Closing

- Get copies of everything

- Change the locks

- Transfer utilities

- File your homestead exemption (for property tax savings)

- Start a home maintenance schedule

Common Mistakes to Avoid

- Shopping for homes before getting pre-approved

- Maxing out your budget

- Skipping the home inspection

- Making emotional decisions

- Ignoring the neighborhood

- Forgetting about ongoing costs

- Waiving important contingencies to compete

- Not reading documents before signing

Your Real Estate Buying Checklist

Use this to track your progress:

- Check and optimize credit score

- Calculate realistic budget

- Save for down payment + reserves

- Get pre-approved (2-3 lenders)

- Define priorities and deal-breakers

- Interview and select agent

- Search and tour homes

- Make offer on chosen property

- Complete home inspection

- Review all disclosures

- Negotiate repairs/credits

- Final loan approval

- Closing disclosure review

- Final walkthrough

- Close and get keys!

The Bottom Line

Buying real estate doesn't have to be overwhelming. With proper preparation, a clear understanding of the process, and the right team supporting you, you can navigate each step with confidence.

Take your time on the front end—getting your finances right and understanding what you want. Move decisively when you find the right property. And never let the excitement of buying override your judgment on the fundamentals.

Your future home is out there. This guide gives you the roadmap to find it.

Want help understanding your specific property? Upload your disclosure documents and get AI-powered analysis of potential risks and issues before you commit.