How to Read a Home Appraisal Report

Understanding your appraisal report so you can negotiate smarter and avoid overpaying. Your AI-powered guide to home buying.

You've agreed on a price with the seller, your lender ordered an appraisal, and now you're staring at a dense report full of numbers and checkboxes. What does it all mean? And more importantly, does it affect your deal?

An appraisal is an independent opinion of a home's market value. Lenders require it to make sure they're not lending more than the property is worth. But for buyers, it's also a powerful tool for understanding what you're actually buying.

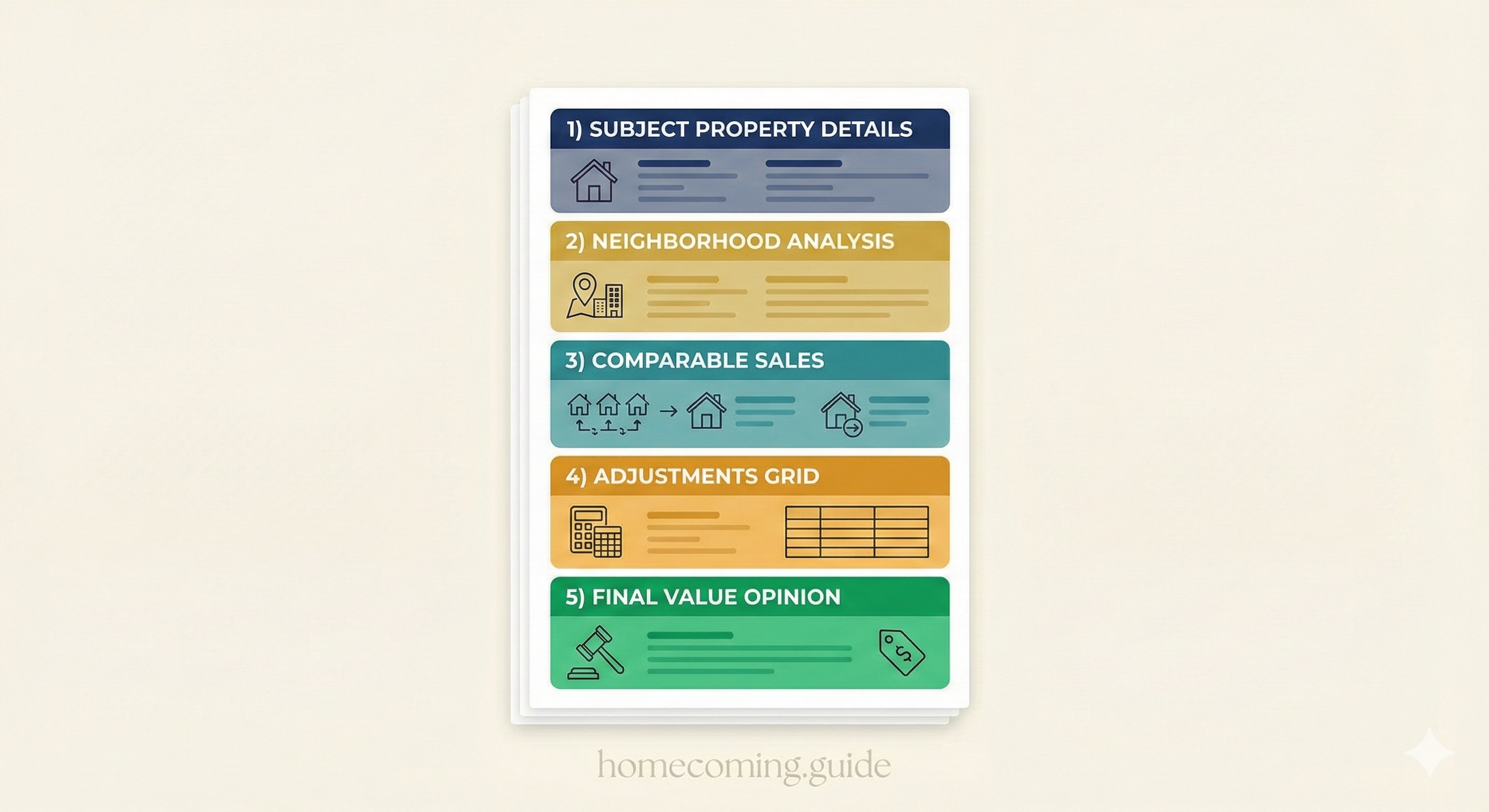

The Three Parts of Every Appraisal

1. Subject Property Description

This section details the home being appraised:

- Property address and legal description

- Property type (single-family, condo, etc.)

- Year built and effective age — Effective age reflects condition, not just calendar years

- Gross living area (GLA) — Above-grade finished square footage

- Room count — Bedrooms, bathrooms, total rooms

- Site details — Lot size, view, location factors

- Construction quality and condition ratings

Pay attention to: Discrepancies between the listing description and the appraisal. If the listing claimed 2,000 square feet but the appraiser measured 1,850, that's significant.

2. Comparable Sales Analysis

This is the heart of the appraisal. The appraiser identifies 3-6 similar properties that recently sold nearby and adjusts their sale prices to account for differences.

| Factor | Adjustment Example |

|---|---|

| Square footage | +/- $50-150 per sq ft difference |

| Bedrooms/baths | +/- $5,000-15,000 per room |

| Garage spaces | +/- $5,000-20,000 per space |

| Lot size | Varies by market |

| Age/condition | Based on effective age comparison |

| Upgrades | Kitchen, baths, finishes |

After adjustments, the comparable sales should cluster around a similar value. If they're all over the map, the appraisal might be on shaky ground.

3. Final Value Conclusion

The appraiser weighs all the data and arrives at an opinion of market value. This number determines how much the lender will finance:

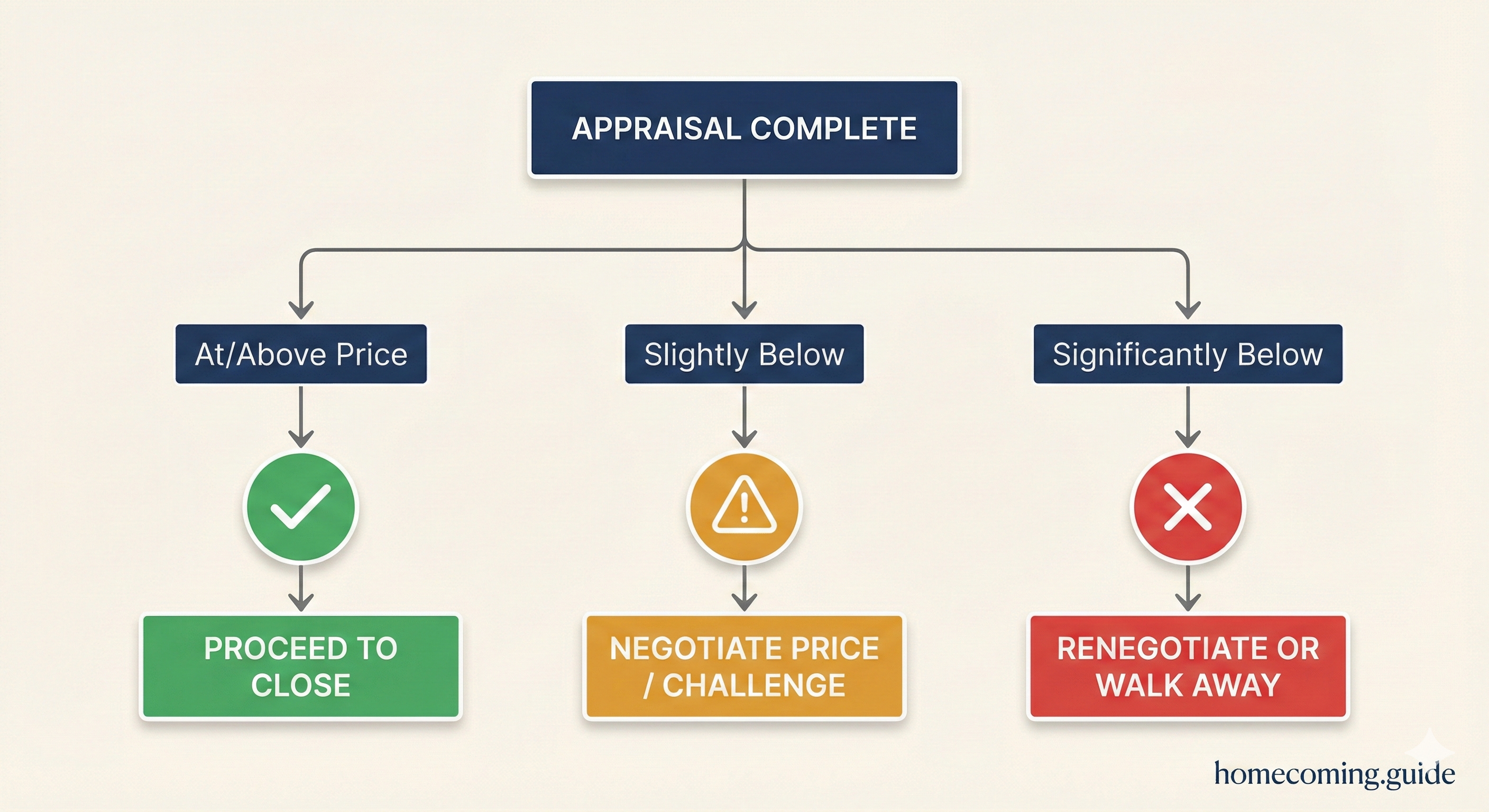

- At or above purchase price: You're good to proceed

- Below purchase price: You have a gap to address

What the Condition Ratings Mean

Appraisers rate both construction quality and condition on a scale:

Quality Ratings (Q1-Q6):

- Q1-Q2: Custom, high-end construction

- Q3-Q4: Standard to good quality

- Q5-Q6: Basic or below-average quality

Condition Ratings (C1-C6):

- C1-C2: New or like-new, no repairs needed

- C3-C4: Well-maintained, minor wear

- C5-C6: Significant repairs needed, deferred maintenance

A C4 or C5 rating isn't necessarily bad—it just means you should factor maintenance costs into your planning.

When the Appraisal Comes in Low

A low appraisal doesn't kill a deal, but it does create a gap between what you agreed to pay and what the lender will finance. Your options:

Renegotiate the price. Show the seller the appraisal and ask them to reduce the price to match. In a balanced market, this often works.

Pay the difference. If you have extra cash and believe the home is worth it, you can cover the gap out of pocket.

Challenge the appraisal. If you believe the appraiser missed comparable sales or made errors, your lender can request a reconsideration of value. Provide specific comps that support a higher value.

Walk away. If your contract has an appraisal contingency, a low appraisal is valid grounds to exit the deal with your earnest money intact.

Red Flags in Appraisal Reports

Watch for these warning signs:

- Comps from far away or long ago — Should be within 1 mile and 6 months when possible

- Significant adjustments — If comps require $50,000+ in adjustments, they may not be truly comparable

- Condition issues noted — Read the comments; appraisers often flag concerns about deferred maintenance

- Functional obsolescence — Outdated layouts or features that hurt marketability

- External factors — Nearby nuisances, traffic, or adverse conditions

Using the Appraisal as a Buyer

Beyond the number, the appraisal gives you information:

Market context. The comparable sales show you what similar homes actually sold for—useful for knowing if you're getting a fair deal.

Property details. Square footage, room counts, and site information are professionally measured and documented.

Condition insights. Appraisers note visible defects, deferred maintenance, and factors affecting value.

Negotiating leverage. If the appraisal supports a lower value, you have objective third-party evidence for price negotiations.

The Bottom Line

An appraisal protects both you and the lender from overpaying. Read it carefully—not just the final number, but the details about the property and how the value was determined. If something doesn't look right, ask questions. The more you understand about the report, the stronger your position in negotiations.

And remember: an appraisal is an opinion of value at a specific point in time. Markets change, and so do property values. What matters most is whether the home works for your life and your budget, not just what one report says it's worth.

Understand Every Document—Not Just the Appraisal

Your appraisal is just one piece of the puzzle. The disclosure documents reveal issues that affect both value and livability. Homecoming—your AI-powered home buying advisor—analyzes your disclosures to give you the complete picture.

Buy Smarter. Buy Confident. Upload your disclosure and get instant insights that put you in the driver seat.